Market Overview

2022 was a rollercoaster year that saw war between Russia and Ukraine, fears of an energy crisis, surging inflation, and central banks raising interest rates at a pace not seen in decades.

While it’s impossible to summarize a year in just a few sentences there are several points from 2022 worthy of note:

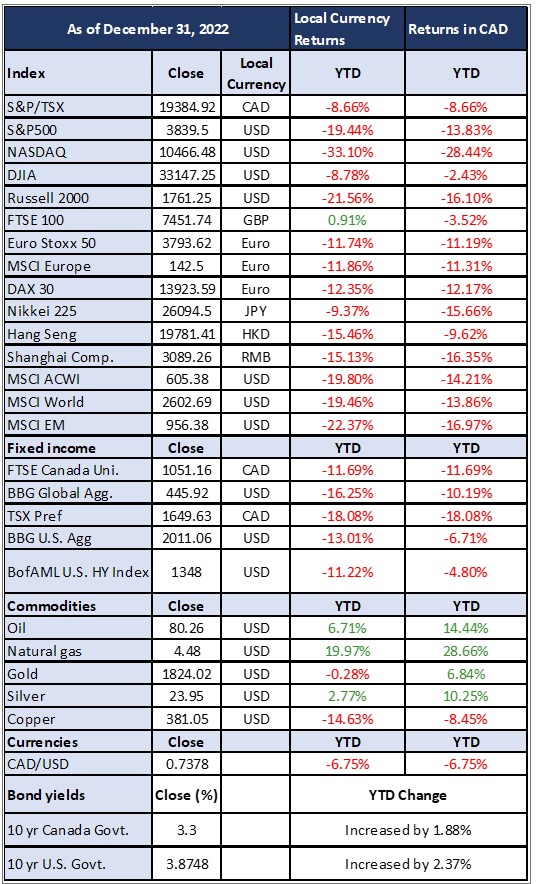

- Stocks had their worst year since 2008. Bonds had their worst year on record.

- Market movements continued (and will continue) to be driven by the expectations versus realities of interest rate changes.

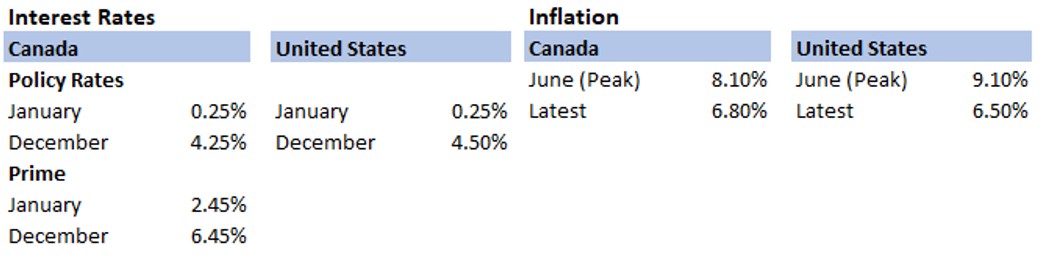

- Inflation rates in Canada and U.S. appeared to have peaked and have continued, albeit slowly, to come down.

- Recession concerns will continue to be top of mind as we wait on whether central banks can avoid inflicting additional hardship.

- The conflict between Russia and Ukraine, while tragic, has become less of a concern for the market in the latter half of the year.

- Economic activity has been slowing, and some countries are likely in a recession today, but others remain reasonably healthy.

- Commodities remained one of the few bright spots for the year, helping the Canadian market outperform many peers.

While some of these worries will continue to drag markets, no one can know for sure how exactly 2023 will look when it’s all said and done. Our views continue to be cautious, but we are increasingly seeing long-term opportunities when looking at all the volatility being experienced globally.

Year to Date Returns

How did you do?

Do-it-yourself investing became a well talked about phenomenon during the early days of COVID lockdowns. Established financial news outlets found themselves reporting on the success of “meme stocks”, NFTs, cryptocurrency, and the larger than life individuals behind these risky endeavors. Have you ever wondered how these same investors did in a year when not everything went up? We did, and fortunately, we were not alone.

According to data compiled by Vanda Research, the average active amateur investor suffered losses of approximately 30% in 2022. JPMorgan Chase & Co. was even more downbeat about these amateur traders, estimating they saw losses of 38%. (Retail Traders Lose $350 Billion in Brutal Year for Taking Risks – Bloomberg)

Even the traditional balanced portfolio of 60% stocks/40% bonds was down over 15% at its lowest in 2022 and finished the year down over 11%.

While no one likes to see the dollar value of their portfolio decline, we think these figures and the ones in the market returns chart seen above pose an important reminder of what value working with an experienced team can provide.

While each individual portfolio is unique and depends on many different factors, we have been very happy with how our clients have fared in 2022. Our outperformance relative to the broader markets can largely be attributed to:

- Our continued focus on active risk management,

- Taking emotion out of the decision-making process,

- Exposure to energy markets in most portfolios,

- Developing a well-diversified portfolio that can withstand the ups and downs of the market, and

- Our inclusion of alternative investments with less correlation to public markets.

Why the next 10 years won’t look like the last 10

The last bull market was 13 years in the making and born out of the Great Financial Crisis of 2008/09. This recession was a difficult time for many reasons outside the scope of this commentary but what is important is what came afterwards:

- Consumers significantly lowered their debt to disposable income (unless you were Canadian).

- We saw persistently low inflation and slow economic growth. This allowed central banks more leeway to stimulate the economy and drive asset prices higher.

- Markets enjoyed strong and steady gains. Companies were able to borrow at next to nothing and investors bet on companies they assumed could grow exponentially in this new normal.

For years investors, economists, and bankers speculated when this bull market would come to an end, but no one foresaw a global pandemic as the underlying reason. A pandemic that drove the excesses of the previous decade to new highs, buckled supply-chains, and finally showed that inflation would not be low forever. We have discussed several times this year that while we believe inflation has likely peaked and will continue to come down from its highs, it is likely to remain well above the central banks 2% target to which they have become accustomed.

What does this mean moving forward?

- Central banks won’t be able to act as freely. Interest rates will rise and fall but are not likely to reach their previous lows any time soon.

- Households and companies will need to rethink their spending.

- The market should still trend higher over the long run, but the highs and lows will be more abrupt.

- The “winners” of the last decade are not certain to be the winners of the next decade. You can’t drive a car looking in the rear-view mirror. Buying something simply because it is down 30+% does not mean it is a good investment.

- Technology stocks provide some history. Prior to 2022, tech stocks grew to become 30% of the S&P 500 and every time an industry has been 30% of the S&P 500 it has then underperformed the next 10 years.

- We analyzed a winner from the early 2000’s tech bubble earlier in the year: TriDelta Financial – Market Commentary for June 2022

Much of this probably seems ominous, but if anything, it has only made us more excited for what’s to come. Will there be difficult years like 2022? Yes. But with each period of volatility there is far more opportunity for the long-term investor than the short-minded trader. We think the value of working with an active manager will be increasingly important moving forward. We are not only investment managers, we help to manage emotions so the households we work with can keep their long-term goals in focus. The risk of a market correction in our mind is not that portfolios have declined but that a client sacrifice achieving their goals in favour of short-term comfort.

The value and importance of financial planning alongside investment management

These days, it can be downright depressing watching the news too closely. Depending on which news source you watch, it is hard not to get despondent. Often, the cure for this is to step far back and look at your personal situation, your immediate world, and not get so worried about the global issues that you can’t control.

We find that financial planning becomes even more important in times like today as it allows you to focus on your world much more than the big, bad world. Just like stepping away from the online news, to focus on your smaller world, a financial plan review allows you to get a better handle on how you are doing, and any adjustments you can make in your world to better align with your goals.

By looking at your taxes, debt, income, estate planning and insurance, it allows us to put your investments in context with your overall picture, goals and plans. This can help us to manage not just the ups and downs of the investment market, but the risk required to meet your overall goals.

What we are doing and why

A couple of weeks back, Ted Rechtshaffen, President & CEO of TriDelta Financial wrote a featured article in the Financial Post discussing his thoughts for what’s to come in 2023. It provides an overview of the world as we currently see it, and we think may come about in the year ahead. In case you didn’t see it, we are providing a link here.

23 investing and personal finance thoughts for what’s to come in ’23 | Financial Post

Stocks/Equities

Worries remain that central banks will raise interest rates too high, and a severe recession will follow. On the other side, worries are central banks will not do enough or governments will introduce stimulus too soon which will prolong the issues and do little to bring down inflation. Both scenarios will have material impacts to investment portfolios but there’s a case to be made that a recession could be the optimal outcome in terms of facilitating a sustainable path towards long-term growth.

Historically speaking, a central bank induced recession is easier to rebound from than a structural failing like what we saw in 2008/09. If a short and mild recession gets the economy back on its low-inflation track, that could be preferable to a world in which high inflation persists for years.

We have mentioned all year that markets are not likely to sustain a prolonged uptrend until we have greater clarity around the path of interest rates. Heading into 2023, the path of markets hinges, as always, on economic growth, corporate profitability, and — most importantly — whether inflation abates, and we can stop raising interest rates.

As we have already written, the last 10 years are very unlikely to simply be repeated when markets finally recover.

- The last cycle centered around growth-oriented stocks (i.e., tech) while the next cycle is likely to be focused on high-quality companies with stable and growing cash flows, often paying a dividend and trading at a much more reasonable level than some of their high-growth peers.

- With inflation being more elevated, the winners and losers in this environment will depend on those that can better contain costs.

- We continue to expect Canada to perform well in comparison to global peers. Canada was a relative stand out in 2022 with economic growth likely finishing in the 2.5%-3% range.

- We are not simply looking for companies trading at discounts relative to their pre-2022 highs. Some companies are justifiably down. Companies with poor debt management, inexperienced management teams, and slim cash flows should likely be avoided.

- Both TriDelta equity funds continue to use cash tactically to take advantage of significant price swings as we expect to remain cautious in the first months of 2023.

- Areas we like moving forward include:

- Healthcare – the population isn’t getting any younger. Healthcare is the third-best performing industry of all time, and it has just come off a three-year period of underperformance.

- Energy – despite the recent volatility there remain a lot of strong fundamental reasons to be confident in energy. There are also a lot of uses of oil and gas for which there is no substitute such as plastics, vitamins, fertilizer, drug ingredients, flavors, and fragrances.

- Globally (outside of North America), markets have seen meaningful selloffs and are often trading at much better valuations than their U.S. peers, creating an attractive entry.

- Emerging markets pose an attractive entry point at current levels. A potentially weakening US dollar, new optimism around a Chinese reopening, and valuations at extreme lows all bode well for these companies in the near term.

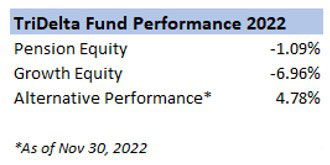

The TriDelta Pension and Growth Funds performed exceptionally well in 2022. The Pension and Growth funds were -1.09% and -6.96%, respectively. Following a strong 2021 where the Pension and Growth funds returned +16.4% and +28.5%, 2022’s performance is evidence to the risk management strategies we employ within the funds and why capital preservation is always an important consideration.

Bonds

As mentioned earlier, bonds had their worst year on record and because of this decline have become a much more attractive space for both income and capital gains. That said, not all bonds are equal and active management will be key to ensuring we take advantage of this asset class in 2023.

Some important aspects to note include:

- There is a broadening belief there will only be one or two more interest rate increases occurring in the first half of 2023 and then subsequent declines in rates as early as the latter half of the year.

- Central banks have been adamant that they disagree with this assessment and do not forecast cutting rates in the second half of the year.

- Key to the future of interest rates will include inflation continuing to fall and a weakening labour market in North America.

- As we saw with the United Kingdom in 2022, government decisions to use fiscal spending to spur growth would likely force central banks to raise interest rates higher than expected.

- Globally, we expect currency changes to be volatile. Much of this change will be influenced by government decisions in the face of declining economic growth. Fundamentally we see the Canadian dollar as lower than what it should be.

- Limited Recourse Capital Notes (LRCNs) have been an important addition to our inclusion in bond portfolios. With yields currently averaging around 7.5% on new issuances, we foresee further issuance into 2023 at potentially even greater yields.

Preferred Shares

Preferred shares ended a difficult 2022 down 20% on the year. Pressure from Limited Recourse Capital Notes and tax loss selling into year-end were significant detractors to close the year. Preferred shares continue to be a space we monitor closely as income yields have continued to rise, yielding 6.3% on average, and investors have benefited owning preferred shares that have been redeemed in 2022 with 15% of the Canadian market being redeemed by issuers.

Alternatives

2022 was a year where alternatives demonstrated a lot of value in client portfolios. Private credit and real estate returns remained broadly strong and have been one of the lone positives in portfolios. We continue to have regular conversations with our managers and have continued to add new funds to our offering.

- Private debt stands as a beneficiary of rising interest rates as they are able to pass along these rates to borrowers and expand their pool of opportunity as more companies are no longer able to seek traditional bank financing.

- Rates on these loans are up 4% in most cases and referrals continue to come from the banks themselves.

- Private real estate has performed much differently than their publicly traded peers. While the impact of rising interest rates is being felt across the space, not all types and geographies of real estate are the same.

- Many of our managers operate in niche markets which has provided insulation from these changing rates while rent increases have continued to climb as the long-term case for rentals persists.

In Conclusion

In five years’ time we see it as a very real possibility we will look at 2022 as a year people look back on as having been a great opportunity for investors. Stocks in 2022 had their worst year since 2008 while bonds had their worst year ever recorded. We know first-hand that there is no one on our team who would say they wouldn’t go back in time and put everything they could in the market in late 2008 but we also know hindsight is 20/20. We still think there will be ups and downs in 2023 and beyond but having a long-term focus will be what ultimately protects your portfolio and helps you succeed.

If you would like to discuss your financial plan or investment portfolio, please give us a call or send a note.