The second quarter of 2019 has felt a little like Canada’s Wonderland. You climb the roller coaster, then you experience big ‘wind in your hair’ descent, then another climb. At TriDelta, we definitely work to smooth out your portfolio returns much more than the typical stock market, but I am sure that most of you still felt a bit of the roller coaster as you reviewed portfolios online or through monthly statements.

The second quarter of 2019 has felt a little like Canada’s Wonderland. You climb the roller coaster, then you experience big ‘wind in your hair’ descent, then another climb. At TriDelta, we definitely work to smooth out your portfolio returns much more than the typical stock market, but I am sure that most of you still felt a bit of the roller coaster as you reviewed portfolios online or through monthly statements.

While the overall returns for equity markets were positive in the second quarter, volatility returned in May. After the stock market continued its strong year-to-date returns in April with the S&P500 (US) rising by 3.9%, the S&P/TSX Composite (Canada) increasing by 3% and Euro Stoxx 50 (Europe) up 4.9%, May saw the reversal of fortunes with the S&P500 declining 6.6%, TSX dropping 3.3% and Europe down 6.7%. June returns were positive again at +5% for the S&P500 (although only 1.8% in Canadian dollars due to a 3% increase in CAD during the month), +0.5% for the TSX and +3.7% for Europe.

Bonds performed well with the FTSE TSX Bond Universe index rising by 2.55%. during the quarter with much lower volatility than the stock market (bonds have sold off a bit so far in July). Preferred shares continued to struggle, with the BMO 50 Preferred Share index declining by 2.4% in the quarter, but have performed well recently with a 0.5% rise in June and so far +1.5% in July. Preferred shares continue to offer high tax-efficient dividend yields, especially relative to other income investments. If bonds prices stabilize, preferred shares could also enjoy some capital gain. For more information on the Preferred Shares market, the reason for its decline, and the opportunity for positive future returns, please click here.

While declines can be stressful, even during periods of overall rising equity markets, it is worth remembering that equity markets have typically provided higher returns than most other asset classes, particularly bonds, but with much higher volatility. Even though equity markets (as represented by the S&P500 in the US) have generated positive calendar year returns roughly 70% of the time, in a typical calendar year, equity markets experience declines of 5% or more 3 times and one decline of 10% or more.

TriDelta clients on average were up between 0.25% and 1.5% during the quarter with the biggest difference being the percentage exposure to Preferred Shares. Our basket of alternative investments continued to perform in line with expectations, with private debt funds up approx. 2%, mortgage investment funds up 1%-2% and real estate up 2.5%, outperforming stocks.

So the key question for most investors is why the strength in April and June vs. declines in May? And more importantly, are we in for weak equity markets like we experienced in Q4 2018 when the S&P500 fell 20% from its peak before recovering? Or can we expect strong market conditions, like Q1 2019 when nearly all major markets were up at least 10%?

Earnings, valuations, cash flows and growth rates should ultimately dictate long-term returns for investors. In fact, most classic equity and market valuation models are based on trying to forecast future earnings and cash flows from an investment based on growth rates, but also bond yields. Sometimes, short-term declines are the result of seasonal factors, or major headlines, such as the continued trade discussions between US and China and in May the threat of US tariffs on Mexico. Often though there may be no clear reason for short-term declines. But in recent years, accommodative monetary policy has definitely been a factor in the strength of (and sometimes weakness in) the equity markets.

Why Central Banks Matter?

Central Banks main goal is to use monetary policy (primarily by setting government interest rates, but also by buying and selling government or related bonds in the market) to keep inflation at stable, predictable levels (price stability). The US central bank, the Federal Reserve, actually has two mandates of price stability and full employment.

Since 2008, central banks lowered interest rates to unprecedented levels and even engaged in quantitative easing, buying long dated bonds, to lower longer-term interest rates. The actions of central banks influence money supply, bond yields and even overall economic growth as more flexible monetary conditions can help protect companies and investors. Companies with higher levels of debt can more easily pay and finance credit. Lower borrowing costs can increase profits for corporations and can be used for dividend increases or share buybacks. Lower rates also encourage individuals and endowments to invest in riskier assets when holding cash that offers only meager returns. Higher dividend paying equities appear more attractive in a low yield environment as they offer higher yields than bonds with the potential for upside (they also have the potential for downside if prices drop). Higher valuations seem more reasonable in an environment of low rates, so stock prices go up and investors seeking higher returns bid up growth stocks.

The Q4 2018 sell-off was impacted by fears of slowing growth, a breakdown in US-China trade discussions, but also due to more hawkish central banks. In fact, when the US Federal Reserve (the ‘Fed’) raised rates in December, then commented that it expected future interest rate increases AND expected further reductions in its bond holdings, this threw fire on an already nervous equity market, accelerating declines in stocks, before recovery began just after Christmas.

Presently, US President Trump is demanding that the Federal Reserve reduce rates, Wall Street is anticipating a rate cut later this month AND at least two more rate cuts within twelve months. If this were to occur, the Bank of Canada, which has been neutral, would have to lower rates as well or see the Canadian dollar rise significantly due to the higher yield of Canadian bonds vs. US bonds. The problem is that while yes the world’s growth rate is slowing and lowering rates would help spur growth, most US economists do not see the need for rate cuts. They still anticipate GDP growth of over 2% in both 2019 and 2020, slower, but still a good growth rate for an advanced economy ten years into a recovery. They expect the unemployment rate, already near historical lows, to decline even further, and for inflation to be slightly above 2% (the Fed’s target rate), so these economists do not see a need for near-term rate cuts. (Source: Blomberg Economics, July 8, 2019). Most members of the Federal Reserve are economists. So who will win? Wall Street and the President or the more conservative economists? Much like the Kawhi Leonard watch to determine which basketball team he signed with, the Fed’s decision will also be followed and analyzed throughout the summer.

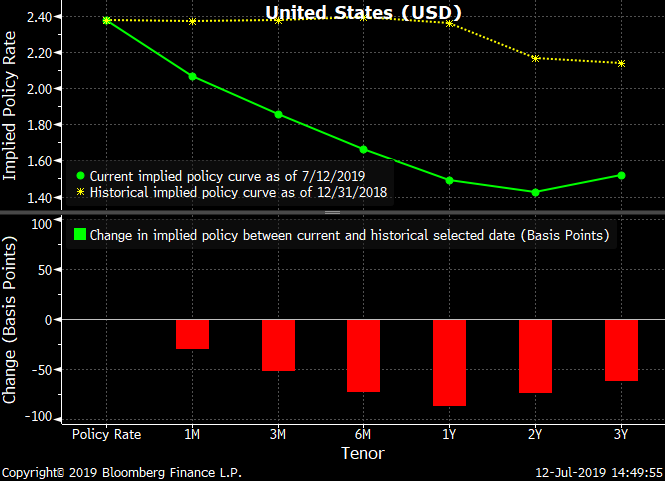

US Federal Reserve Interest Rate Expectations

The green line reflects the projected Federal Funds Rate (interest rates) per members of the Federal Reserve at July 12, 2019. The yellow line reflected those projections at December 31, 2018. For example, at the end of 2018, the Fed expected rates to stay at approximately 2.4% in one year’s time and now expect rates to be closer to 1.5% over that period.

At TriDelta, we think the result is likely to be somewhere in the middle. We will get at least one rate cut in 2019, but possibly later than July and we may see only 1-2 additional cuts within the next 12 months. If this is the case, Wall Street is likely to be disappointed and we could be in for a few months of volatility.

As a result, we have focused equally on capital preservation as well as growth. The stocks currently in the equity portfolios have higher yields than the overall market, as well as lower volatility (Beta) and cheaper valuations (as measured by Price / Earnings ratios). We also presently hold higher levels of cash in our equity funds. Our bond portfolios hold shorter terms to maturity than the Canadian bond universe and has improved its credit quality. We also continue to believe that investing a portion of clients’ portfolios in income-focused alternative investments should provide less volatility and a higher level of income than a typical stock and bond only balanced portfolio.

We will continue to monitor market conditions, particularly leading indicators, developments in trade discussions and their impact on the world economy, as well as technical factors that may give indications of potential market movements and which sectors to favour.

Update on Private Investments

At the end of Q2, both TriDelta Fixed Income and High Income Balanced Funds made additional distributions based on investments being sold or maturing. Distributions for the Fixed Income Fund were roughly 0.5% and just over 13% for the High Income Balanced Fund. Additional distributions are expected near the end of Q3 as certain bonds mature and others are sold.

Summary:

We continue to search for value in under covered areas of the market, such as a promissory note issued by a leader in the litigation finance field that pays our clients a 10% yield, as well as stocks, preferred shares and bonds trading below historical averages or offering higher levels of growth than are priced in by the market. We are also focused on capital preservation, income and reducing overall risk through prudent management and diversification.

We hope that you have a chance to enjoy the sunshine and good weather that we are presently experiencing. Summers in Canada are too short, so they must be savoured.

TriDelta Investment Management Committee

VP, Equities |

President and CEO |

Exec VP and Portfolio Manager |

VP, Portfolio Manager and |