Market Overview

2025 was a year of uncertainty. Whether it was tariffs and rapidly changing trade relationships, fears of an artificial intelligence (AI) bubble, or geopolitical tensions, investors had a lot to consider. Despite everything, it was a remarkable year for equities, and the final months proved a continuation of the rally which followed the tariff driven negativity early in the year. Virtually all major markets rose in 2025, but the real winners were stock markets outside of the U.S. which outperformed for only the second time in the past 15 years.

In this review we will share our thoughts on the lingering uncertainties of 2025 and the investment themes which may drive returns in 2026.

- U.S. equities staged a remarkable comeback after falling nearly 20% in April, but international markets were the largest contributor to global returns.

- Despite trade uncertainty, Canada pushed record highs with the TSX posting its best return in over 15 years.

- Most central banks, including Canada, view interest rates in a good place entering 2026. The U.S. is a notable exception which was on hold most of the year and is expected to bring rates down in 2026.

- Earnings in Canada and the U.S. have remained strong, which has helped justify the increasingly expensive valuations being assigned to stocks.

- While high valuations – as measured by a market (or company) price-to-earnings ratio – do not signal the future, it does increase risks of a misstep should expectations not meet reality.

- After falling nearly 11% during the first half of the year – as measured by the USD Index – the U.S. dollar stabilized and recovered modestly in the latter half of 2025.

- The Canadian dollar mildly outperformed but remains close to the weakest among the major currencies.

- Investors once again view the potential for global conflicts as a top risk for 2026.

- International attention paid to various crises around the world grabbed headlines throughout the year but proved only short-term volatility.

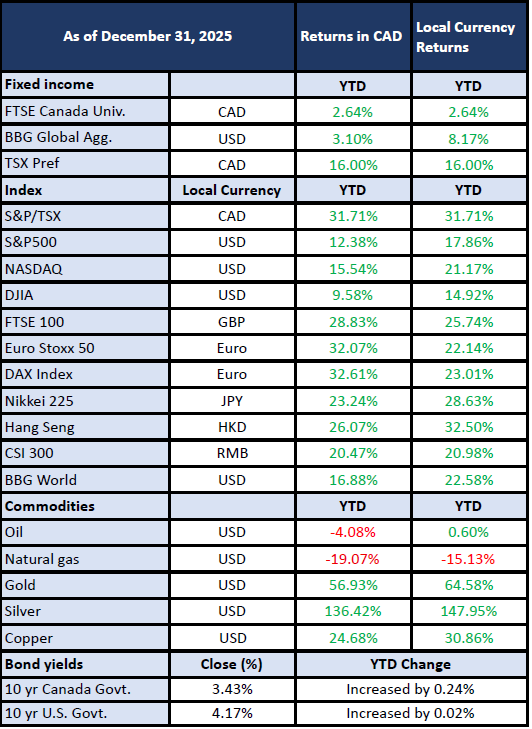

Market Returns

What to Expect in 2026

As we move deeper into the new year, the uncertainties of 2025 will persist, but investors will be hoping to look back on 2026 as the year of resilience. The logical question investors have is whether markets can follow up on an already incredible three years. Some think so. Outlook reports from wealth and asset managers point to lower interest rates, government spending, and the ongoing building out of Artificial Intelligence (AI) as factors that will keep momentum into 2026. While there are reasons to be optimistic about the year ahead, there may be different narratives which drive returns and the path is unlikely to be straightforward.

Taking a look at some of the major themes, there remains a lot for investors to consider.

U.S. Equities & the AI “Bubble”

Concerns of an AI bubble have captured the attention of investors and the pressure on companies to prove AI can pay off in the real world will define 2026. While not the same as the Dot Com era of the late 1990’s, the release of ChatGPT in November 2022 may be used as a reference point for the AI bubble should a true boom and bust cycle truly materialize.

There are two sides to this talk of a bubble, however it should be noted that any true bubble is characterized as a period where investor optimism and enthusiasm overcome any sense of long-term reason in the prices people are willing to pay for those companies. Another key trait is often the fact that bubbles are only really known in hindsight. With that in mind, if investors are even speaking about a bubble, wouldn’t that mean people are not overly optimistic? It’s hard to say but like many others, we’re still cautious about where valuations have climbed.

Regardless of your thoughts on AI as an investment or as a tool, it is not going away.

- The AI theme is big and it’s a primary reason why U.S. markets look increasingly expensive – the top 10 stocks in the S&P 500 account for almost 40% of the index.

- AI stocks are expensive but not quite what we saw in the Dot Com era.

- AI darling Nvidia trades at 45 times earnings, expensive but it’s not the 140 times earnings Cisco was valued at just ahead of the Dot Com bubble burst.

- Expectations are high.

- One way to gauge current optimism about the future is to measure future growth expectations embedded in markets. To this end, the 10-year forward growth implied by the S&P 500’s current market value is now close to 16%, compared to a long-term average of 11%.

- Not as high as the 21% achieved in 2000, but it still represents lofty expectations.

- One way to gauge current optimism about the future is to measure future growth expectations embedded in markets. To this end, the 10-year forward growth implied by the S&P 500’s current market value is now close to 16%, compared to a long-term average of 11%.

- Estimates point to almost $7 trillion in global data centre infrastructure spending by 2030, an amount roughly equal to the combined GDP of Japan and Germany.

- In the first half of 2025, AI related spending contributed as much as consumer spending to U.S. GDP growth.

As we move forward and AI adoption progresses, companies will need to demonstrate applications for how AI is improving their businesses as investors reach the end of their tolerance for being told how great AI is and instead demand companies to show them. If companies can continue to deliver results, then prices may push higher but such little room for disappointment indicates the potential for more down from here.

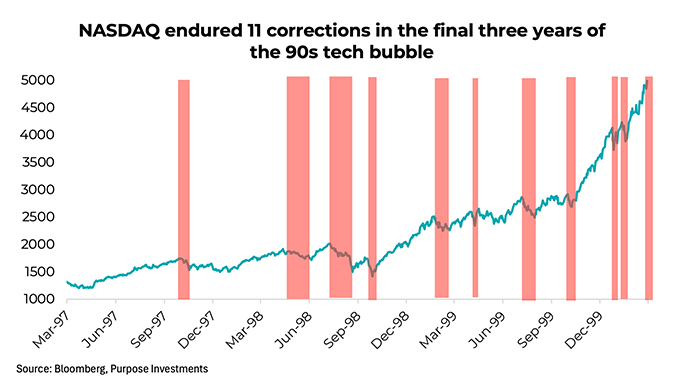

If this is a bubble, perhaps it’s still in the early stages of forming. If that is the case, we would point to the final three years of the Dot Com era in which the tech heavy Nasdaq index experienced 11 declines of 10% or more on its way to increasing 300% cumulatively.

International Markets & the Case for Diversification

2025 was an example of how diversification can be important and why trend following can lead to wide swings for investment portfolios. While U.S. outperformance has been nothing new over the prior decade, the post-COVID era can be attributed largely to AI dominance and increased government spending to support markets and consumers. This differs from many international peers as nations coming out of the pandemic reigned in spending to bring down deficits. In 2025 this changed dramatically for a few reasons.

- The U.S. trade war,

- Europe’s new reality without U.S. defense support,

- A weaker U.S. dollar helping with the competitiveness of many emerging markets.

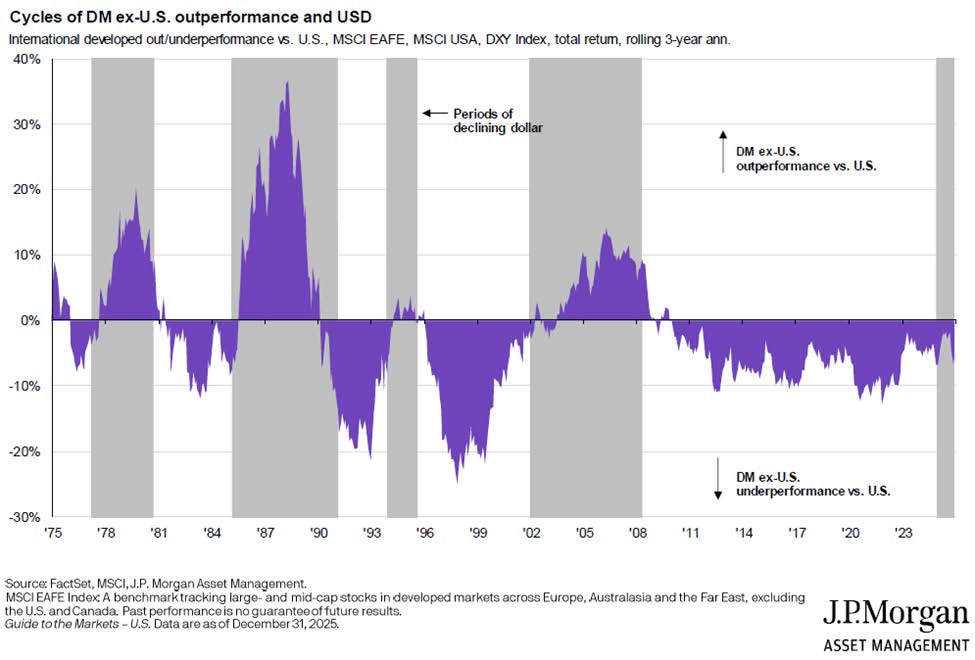

Investors have seen periods like this before, when international markets appeared poised to overtake the U.S. for an extended time. Instead, the past decade has seen many false starts. The below chart shows periods of U.S. versus non-U.S. outperformance. As you can see, the U.S. has had an extended run of gains relative to international stocks.

There are notable differences today which may help continue the success of international markets.

- Europe’s new reality of less U.S. participation in their defense is equating to billions of new investments in their defense capability and infrastructure.

- Japan too, announced its biggest ever government spending package (outside of COVID) in decades.

- European consumers are sitting on substantial excess savings and limited debt which, coupled with lower interest rates, provides much more support for the European economy.

- Many pro-business corporate reforms are happening in Asian countries such as Japan and Korea.

- Rotation out of expensive U.S. stocks towards more reasonably valued regions.

- Investors are generally still underweight international and emerging equities with most “global” investment funds holding approximately 60% in the U.S.

Ultimately, diversification is one of the best ways to construct portfolios for unexpected market scenarios. This increased diversification benefit coupled with the value opportunity in many international markets, should provide a lift for investment portfolios in terms of returns and, potentially, less downside should markets experience increased volatility in 2026.

Canada & U.S. Tariffs

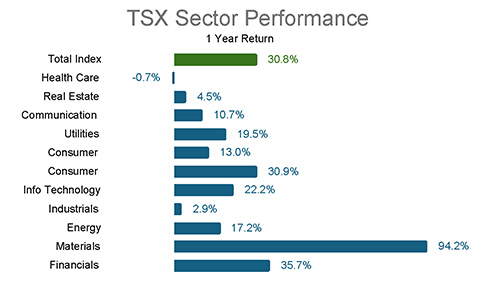

Canada’s TSX Index produced an outstanding return in 2025 which many investors would likely have found surprising at the beginning of the year. Although tariffs were a meaningful detractor from the Canadian economy, the impact was more industry specific rather than the broad-based shock initially expected. This largely allowed investors to re-focus on other stories throughout the year, with the rally in gold stocks, banks, and Shopify carrying the day.

Source: TriDelta Private Wealth, Bloomberg

Although it may not have seemed like it during the year, Canada was largely spared from U.S. tariffs in 2025.

- Most exports to the U.S. remained protected under the USMCA trade agreement signed in President Trump’s first term.

- It is estimated the effective tariff rate on Canada was 3.9% while the U.S. finished the year with average global tariffs between 13% and 15%.

- While investors may have moved on from tariffs, the summer formal review of the USMCA will be a focal point for Canadians in 2026.

- Some form of the USMCA is likely but expect concessions from Canada will drive weakness in specific areas of the Canadian economy.

- The U.S. Supreme Court is expected to rule on whether the Trump Administration’s tariffs are legal, however this is more headline noise.

- The Trump administration have alternative levers they can pull to impose tariffs which we view as the likely scenario should the ruling go against them.

Tariff headlines are unlikely to drive major market moves in 2026 but will be a lingering hurdle for businesses to navigate. After the renegotiation of the USMCA, investors can expect the tariff drama to roll off as the U.S. focuses on other priorities leading up to the U.S. midterm elections during the second half of the year.

Interest Rates

Most central banks, including Canada, view interest rates in a reasonably good place while investors largely expect at least two reductions from the U.S.

Interest rate decisions from the U.S. – as the world’s largest economy and reserve currency – may drive market swings for investors.

- In May, the Trump administration will appoint a new Chairman likely to be in favour of reductions in interest rates. While President Trump’s influence will be top of mind, the Chairman counts for one vote of a 12 person committee.

- Investors and policy-makers also appreciate the costs of being too aggressive with interest rates:

- Weaker U.S. Dollar (USD) – further weakness in the USD would likely be viewed as a positive by some as U.S. exports become more competitive but would reduce investment returns in U.S. assets.

- Higher Bond Yields – this could be a significant consequence for the U.S. by way of bond market volatility and challenge investment returns in stocks.

- Investors and policy-makers also appreciate the costs of being too aggressive with interest rates:

- Of particular interest will be the continued encroachment of U.S. Fed independence which is viewed as a pillar for global financial stability.

Global Tensions

We wrote about geopolitics a year ago as most investors viewed it as their top concern moving into 2025. One could certainly argue as having been right given the number of headlines and international attention paid to various crises around the world but, for the most part, markets moved on quickly as far as global conflicts were concerned.

Like the several other events of the prior few years, the U.S. capture of Venezuelan President Maduro is unlikely to be a major market mover unless the scope of the conflict intensifies. The primary concern markets may be looking for is the reaction of China given the oil China utilizes from Venezuela, potential justification for a reclamation of Taiwan, or restrictions put on Chinese exports of rare earth minerals essential to the AI theme dominating investment markets.

While there will likely be other events in 2026 which drive headlines and investment volatility, investors should be reminded that reactions to otherwise negative news can lead to some expensive investment mistakes.

What we are doing and why

Stocks

The final months of 2025 ended positively and capped off a remarkable year for equities, albeit, with greater volatility as investors rebalanced away from the expensive AI trade. Both TriDelta strategies demonstrated exceptional performance throughout the course of the year and did so while maintaining a disciplined process for investing in businesses we understand, trade at a reasonable valuation, and have a long runway for growth. Interestingly, the TriDelta Growth Fund achieved an annualized return of nearly 24% these past three years without holding any of the “Magnificent 7” stocks. While investment markets, particularly those in the U.S., remain highly concentrated in large, often, AI-related businesses, we have sought to invest differently and towards achieving favourable returns with less volatility than the overall market.

Over the next several years we continue to think investment returns will be very different among major markets compared to those experienced in recent years. This is particularly true if we see rotation away from the expensive areas of the market (technology/AI) and towards other sectors and regions. With that in mind, we argue in favour of being highly selective in the businesses we invest and having a disciplined process for risk management.

For an update on our current positioning, you can learn more about our strategies here:

Bonds

Attitudes in the bond market improved due to improving inflation, lower interest rates, reasonable economic growth, and improvement in the finances of the U.S. government which provides the foundation for the world’s largest bond market. Despite the better tone, the tighter spreads mean investors are often not adequately being compensated for the associated risk. For this reason, we are focused on investment grade corporate bonds with a shorter term to maturity.

- Most central banks are likely done with interest rates for the time being. A notable exception is the U.S. Federal Reserve which is expected to bring rates down 0.75% to 1.00% from here.

- The potential for lower economic growth and a worsening labour market from the USMCA uncertainty could put a stop to any increase in Canadian interest rates until the economy is on better footing.

- Government support among many nations should provide meaningful short-term support to growth and contribute to a healthier consumer.

- Corporate bond spreads – the difference between corporate and government bond yields – remain tight, reflecting that an economic downturn is not the base-case scenario for investors.

- Any spread widening is likely to be limited unless markets experience a large unforeseen event which reintroduces risk to the bond market.

Commodities

Significant gains could be found in several commodities throughout the year and have acted as a strong diversifier for investment portfolios.

- Metals experts have identified several key drivers behind this upward momentum, with supply disruptions, USD weakness, surging AI infrastructure, and the green energy transition as important factors supporting prices.

- Gold (+64%) was the story of the year, but silver (+148%) quietly saw sizable gains due to supply constraints amid rising industrial demand and its designation as a “U.S. critical mineral”.

- Uranium had a positive but volatile year which is generally favourable for Canada, being the world’s second largest producer.

- Prices are surging as the U.S., Europe, and Asia rush to secure long-term supply to fuel power plants, which is increasingly seen as a solution to climate change and power for data centres.

- The conditions for an oversupplied oil market persist as OPEC/Saudi Arabia unwind prior production cuts to regain market share, normalize spare capacity, and reinforce strategic ties with the U.S.

- Recent developments in Venezuela pose another challenge for oil however it’s unlikely full production could be achieved there for at least 5 years.

- Despite the recent negativity, the lack of projects financed over the past few years should help bring the market into better balance.

Preferred Shares

The overall shrinking availability of preferred shares was met with several new issuances that were quickly absorbed by investors, although the final months of the year still saw net redemptions driving continued positivity. There remain pockets of richly priced preferred shares which we advise avoiding, specifically high-quality rate-resets, but the likelihood of redemptions by traditional bank issuers should add to the continued rally.

Alternatives

An allocation to alternative assets and investment strategies can benefit diversified portfolios when used over the long-term. Given an increasingly uncertain outlook and high valuations in public stocks, we expect the need for additional diversification to benefit investment portfolios outside of traditional stocks and bonds.

Examples of alternative investments we use in portfolios include:

- Private equity; particularly in global infrastructure assets.

- Private lending to Canadian and U.S. businesses

- Music royalties

- Litigation financing

- Inclusive of law firm lending, injury settlement lending, and estate lending.

- Private real estate

- Inclusive of Canadian and U.S. apartment buildings, student housing, self-storage facilities, and new developments.

Looking Ahead

Portfolios that performed best in 2025 were not the ones that predicted all the twists and turns, but those that were diversified and maintained discipline, proving once again the importance of staying invested through uncomfortable periods. As we look forward to 2026 it is unlikely the path will be a straight line and our message is to not sit on the sidelines. While we can never be certain of what the future holds, we know there will likely be market missteps and noisy headlines which will create opportunities for active, disciplined investment decisions.