TriDelta Monthly Cash Creator Program

How to create new monthly cashflow from your home equity

A great banking strategy for years has been the ability to lock in investors in a five-year GIC at a lower rate than the five-year mortgage rate charged to a borrower. Assuming the mortgage is secured, with very little risk, the bank can lock in what was traditionally a one per cent to two per cent profit for five years straight.

Today, interest rates have presented an even better opportunity for some individual Canadians.

If you have good credit and income, you can now get a five-year fixed mortgage for less than two per cent.

If you only want to pay interest, you can get a secured line of credit for 2.45 per cent. This may not always require sizeable income. In some cases, you can even get an unsecured line of credit for 2.45 per cent if you have solid income and credit.

This is an incredibly low borrowing cost. But if the funds are used to generate taxable income, in most cases, you can deduct the interest costs. If you are in a top tax bracket, that essentially cuts your borrowing cost in half, down to around one per cent to 1.25 per cent.

The question is what can or should you do with access to those funds?

Assuming for the moment that you can access funds at those rates, is there an investment that is appropriate to try to match against the borrowing, just like the banks do?

As it turns out, the interest-rate environment has produced two connected opportunities. For individuals (especially those with considerable home equity), interest rates are exceptionally low. At the same time, many businesses are finding that rates for them have not come down at all. In fact, their borrowing costs in some cases have gone up. How can this be with such low interest rates?

The reason is that the same banks that are lending to individuals at very low rates secured against houses, are a little spooked by the size of their lending books and their overall exposure to a meaningful downturn in the economy. That, along with something called regulatory risk capital, means banks have been less willing to add lending to small and medium sized businesses. As a result, these businesses have to go elsewhere for funds, and while the going rate may be two per cent on a mortgage, the going rate on secured lending to businesses is often over 10 per cent.

These lending rates create what is sometimes called a barbell, where borrowing costs for individuals are very far apart from borrowing costs for many businesses.

What is important is that these aren’t particularly risky businesses, and those that are lending to them have exceptional security on the loans. As a result, the historical loan losses on these business loans have been extremely low.

This brings us back to the question of what you can or should be doing with this access to cheap money.

In our view, if you can match up the cheap borrowing and invest it into secured lending that pays a high rate of return, you are getting close to the security that banks feel when they match GICs with mortgages.

Fortunately, there are now many options to invest with companies that have very strong risk and operational procedures to lend to businesses. These investments have generally had returns for investors in the 6.5 per cent to 8.5 per cent range on a steady basis. We have been using this as part of our investments for clients for about seven years. Even in 2020, the returns stayed very much in line with their historical returns.

This investment strategy will not be for everyone. There is some risk here, but meaningfully less than borrowing to invest in the stock market. In addition, only some people will have the ability to borrow funds.

One example of how this can potentially be used is to create a new monthly cash flow. In some respects it is like creating rental income without the bother of actually having a tenant.

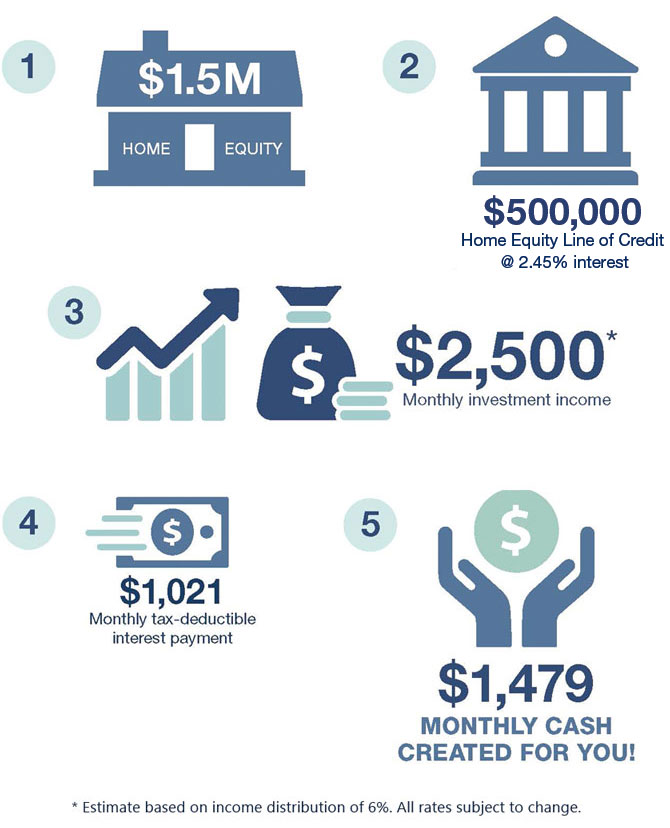

Here is an example of how it would work.

- You own a house worth $1.5 million that either has no mortgage or a relatively small mortgage.

- Using a home equity line of credit at prime, you borrow $500,000 at 2.45 per cent interest. This means that every month you will pay $1,021 in tax deductible interest.

- The $500,000 is invested in a small mix of investments primarily focused on secured lending to businesses, that distribute income monthly. If we use a conservative return number of six per cent, that will generate $2,500 a month.

- Each month, $2,500 a month goes to your bank account a few days before the $1,021 comes out, leaving you with a net monthly cash flow of $1,479. This new monthly cash flow is created using something that is otherwise sitting dormant — the equity built up in your home. The $500,000 invested should remain fairly steady, and hopefully will grow slightly if total returns are over six per cent — as they have been in the private credit space for several years.

While everyone’s situation is different, this is certainly one potential opportunity for many Canadians to increase their wealth and their cash flow, with relatively low risk.

How we produce steady monthly income

TriDelta Financial was founded in 2005, and over the past 8 years, has become one of Canada’s leaders in providing Private Credit investment solutions to investors like you. As some of the largest Pension funds around the world have allocated more money to this space, so have TriDelta clients. They have benefited from diversified returns on Private Credit in the 7% to 9% range most years, with little impact from the ups and downs of the stock market.

Reproduced from the Financial Post, 6 January 2021.