Market Overview

Two major forces dominated the prior three months of 2026: one of the most significant disruptions to energy supply in history and the promise of artificial intelligence (AI). Despite the headlines and concerns over energy security, investors followed company earnings above all else, which proved resilient and were boosted by enthusiasm for AI.

Markets have been impressively resilient to shocks in recent years, most notably around “Liberation Day” last April and this year with developments in the Middle East. We cannot, however, take this resilience for granted. We remain encouraged by the strength in company earnings and believe positioning an investment portfolio with greater diversification and income than the major stock indices currently provide is a necessity to weather what we believe will be more volatility ahead, not less.

In this review we share our perspective on the first half of the year and takeaways for the months ahead.

- Markets have performed well above average and while there will continue to be rumblings of a stock bubble, markets can stay elevated for longer than people anticipate.

- Despite the sharp rise across global markets, stock valuations are elevated but have not pushed extremes; gains have instead been attributed to company earnings and reasonably good economic activity.

- The winners of last year have not carried over to 2026. Investors moved to the companies behind the infrastructure necessary for AI at the same time momentum in precious metals became exhausted.

- Interest rate expectations shifted meaningfully after the introduction of the Iran war. Expectations among most central banks are now for interest rates to rise into 2027.

- Rising inflation may be a bigger risk heading into the remainder of the year.

- The Middle East ceasefire is already showing signs of unraveling, indicating more uncertainty ahead.

- Peace talks should continue, but investors have largely written off the conflict. Any significant escalation or prolonged energy surprise would be unwelcome.

Market Returns

Artificial Intelligence (AI) and Market Concentration

The events of 2026 have tested markets without breaking them and much of the credit is due to the earnings of the largest AI companies and those creating the components necessary for the AI infrastructure being built globally. Despite this dominance, concerns over an AI bubble and the market’s growing reliance on this theme continue to shadow its momentum. The innovations of the day have a long history of attracting investment beyond what near-term returns may justify. This can spark large investment booms like we are seeing today and, while “bubbles” are typically only known in hindsight, the truth may lie somewhere between the AI believers and pessimists.

The earnings growth has been real, but the narrative has shifted.

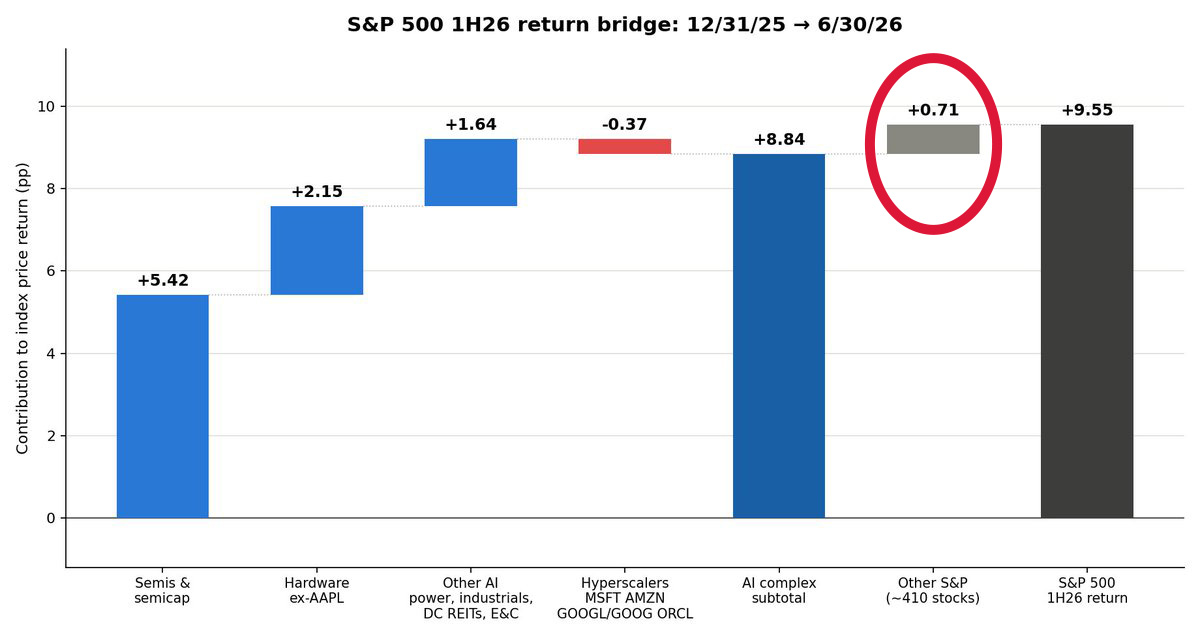

The 2025 winners have not carried the day in 2026 as the companies behind the AI infrastructure have pulled the market higher while the likes of chip-maker Nvidia have trailed behind. The chart below provides a breakdown of the U.S. S&P 500 return contributions to the end of June. Clearly, AI is behind the bulk of returns with non-AI stocks accounting for less than 10% of the total return.

The returns credited to AI companies have been the driving force, pushing markets higher, but this doesn’t tell the full story. Other sectors are growing and producing good returns for investors, but their contribution to the overall index is often negligible.

Semiconductors (SOX Index) are evidence of the shifting AI momentum. These stocks have been the dominant force underlying the latest surge and claimed the AI crown in 2026, far outpacing the Magnificent 7 cohort.

The reliance on AI will determine the direction of broader markets.

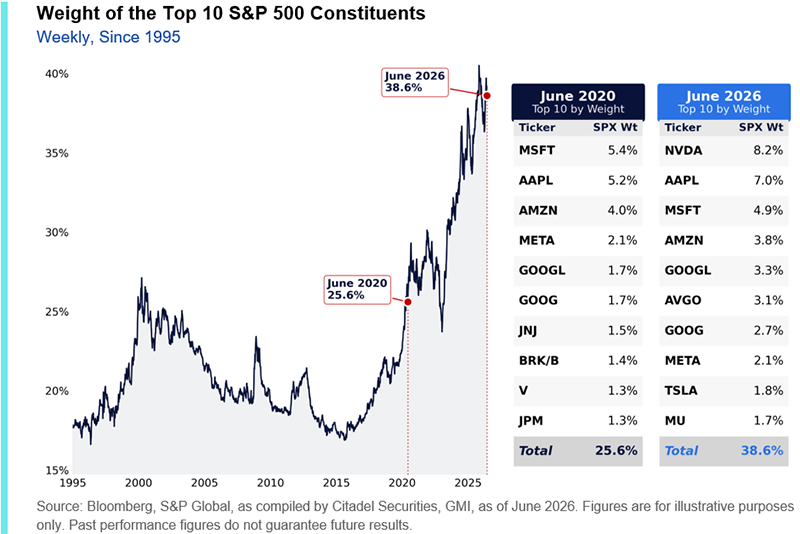

Most stock indices give the largest “weight” to the largest companies. This is true in the U.S. S&P 500 and Nasdaq just as it’s true in Canada’s TSX. The problem is often that the winners take up more of the index until the momentum shifts and another theme takes the day.

Today, nearly 40% of the S&P 500 is in ten companies.

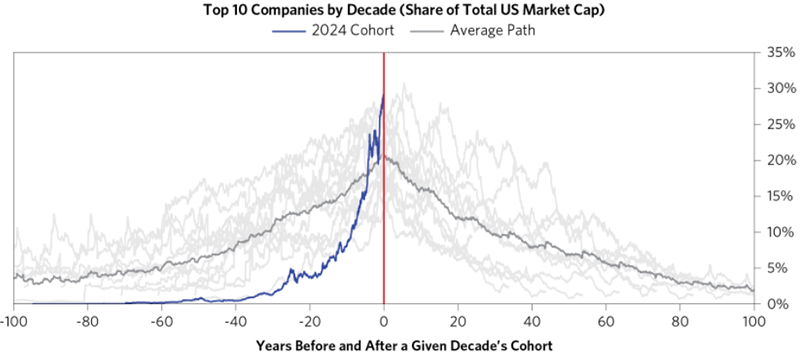

This is elevated in any historical context, and in every other example, new investment themes are right around the corner. The graph below shows the top 10 stocks of each decade and their share of the total market, leading up to and following their peak.

Investors are taking a massive bet that this theme is right. However, we won’t know for years what the return on investment of this AI spending will be and the risk is that, even if the technology fulfills the promise of the optimists, the amount of spending today could yet be overdone, just as internet companies overspent in the late 1990s and early 2000s.

The good news for investors is two-fold:

- No one is forcing anyone to buy passive Exchange Traded Funds (ETFs) which are not providing the diversification or income many need.

- A highly concentrated market means there are less appreciated companies, often priced more reasonably, which are worth our attention.

CUSMA and Canada

The deadline for extending the CUSMA trade agreement has come and gone without a finalized deal between Canada, Mexico, and the U.S.

We now know that the trade agreement will face annual reviews but remain in force until its expiration in 2036. The continued uncertainty is decidedly negative for Canadian businesses as mounting evidence point to private Canadian business investment falling below 2015 levels and lingering headline risk expected to challenge investors.

That said, it’s not all negative.

- CUSMA is still in force and carries the same insulation which benefited Canadian stocks in 2025.

- The trade relationship between the U.S. and Canada is better than headlines are suggesting.

- Mexico has roughly 50 issues to resolve, while Canada has just seven. More issues mean more visible concessions, more progress announcements, more headline momentum, but the pressure on Canada is not what it seems.

- The Iran war and upcoming U.S. election have provided Canada and Mexico greater leverage in the near-term.

- Billions have been spent on the war, inflation is climbing, and U.S. interest rates may be rising all while the Trump administration manages a fragile peace deal. Politics aside, it is not feasible for the Americans to scrap a trade deal with their two largest partners – putting millions of jobs at risk and triggering an effective $466 billion tax increase on consumers.

Investors will be paying close attention to developments moving forward and the risk to Canadian businesses, but the prior year has proven markets’ tendency to overreact to headlines. Given we expect this to continue, it may provide opportunities in individual names and sectors until a deal is reached.

Same Tariffs, New Inflation

Inflation continues to play a central role in shaping expectations. It has remained elevated and above the 2% target set by the Bank of Canada and U.S. Federal Reserve every month for the past five years.

Although rising energy prices have played a role in recent inflation numbers, they were not the only factor.

Throughout 2025, businesses absorbed the bulk of tariff costs rather than passing them to consumers, in part because profit margins allowed it and in part because the U.S. President made clear, publicly and directly, that he expected them to. The result was businesses holding the line, but the Iran war gave companies something they didn’t have before: plausible cover to raise prices.

Rising inflation matters given the difficult spot for consumers facing an affordability crisis at a time when they no longer have the excess COVID savings. Central banks successfully navigated rising inflation earlier in the decade but now have even less room for error given the higher starting point for interest rates which will make this an important investment consideration well into 2027.

What we are doing and why

Stocks

Stock markets have had an incredible run and, although most of the gains have been attributed to AI, the market’s reliance on this theme has helped create under-appreciated segments of the market which we feel offer better long-term value. While others chase returns driven by the fear of missing out (FOMO), we have continued to emphasize income (i.e., dividends) and prudently manage the elevated market concentration through proper diversification, investing in good businesses which carry reasonable valuations, and utilizing various tools for protecting against volatility.

Both the Growth and Pension Funds outperformed broader markets through June as we made several deliberate decisions which benefited our funds in 2026.

- After entering the year more defensive and with elevated cash levels, we took advantage of the early declines associated with the war in Iran by selectively adding to businesses where the impact was overdone or short-sighted.

- Later in the quarter, as AI momentum pushed stock markets to record-highs, we took the opportunity to trim back on several of our AI/technology names such as Micron and Seagate Technology – two primary beneficiaries of AI in 2026.

- This has helped to boost our cash levels and kept our 2026 mantra of being positioned defensively to allow us to act opportunistically throughout the remainder of the year.

Both funds achieved several recent accolades credited to our highly active approach to investing. The TriDelta Growth Fund was ranked as the #1 Canadian Global Equity Fund over seven years while the TriDelta Pension Fund is a top quartile fund over five years with lower risk than its peers.

For an update on our current positioning, you can learn more about our strategies here:

Bonds

Investment returns in bonds remained muted during the quarter but have acted as a stabilizer benefiting from higher income yields than in years past. Our emphasis continues to be in high-quality investment-grade bonds with a shorter time to maturity. We acknowledge this may deliver lower relative returns the longer markets maintain their “risk-on” attitude but feel this offers better value today and greater insultation from the volatility beyond anyone’s control.

- Bonds are still expensive, but investors are becoming more selective. This is evidenced by high-yield (lower-quality) bonds beginning to lag higher-quality, investment-grade bonds.

- We expect this to become more pronounced if/when interest rates rise and general market volatility picks up.

- Interest rate expectations shifted meaningfully after the introduction of the Iran war and continued rise in inflation brought on by energy prices and AI spending.

- Most central banks, including the U.S. Fed, now expect interest rates to rise into 2027. In Canada, where economic growth and CUSMA uncertainty have been negative, the environment for interest rates is relatively more uncertain.

- Elevated inflation is likely to be a major theme into 2027 and carry implications for markets beyond bonds.

Preferred Shares

Canadian preferred shares outperformed stocks through May before ending June in line with the TSX, returning 4.89% in the quarter. In the absence of more sizable redemptions, we expect preferred shares to perform more in line with stocks, while still benefiting from higher income.

Commodities

Despite the longer-term appetite for commodities, the prices of these assets are still subject to the near-term flow of money and supply disruptions that have been evident in 2026.

- The outperformance of precious metals in 2025 has not carried over into 2026.

- The 2025 gains made the metals more reliant on near-term momentum rather than fear or their role as an inflation hedge. Coupled with less concern over U.S. central bank independence, this provided a reset for prices back to more supportive, albeit still higher, levels.

- Energy prices rose and remained volatile throughout the quarter before falling over 30% upon signals of a ceasefire with Iran. While the more recent declines in energy prices were welcome news for consumers and businesses, the geopolitical consequences are still being felt and may lead to a reordering of supply chains creating a higher ‘floor’ price moving forward.

The volatile 2026 for commodities has not changed the underlying story: catalysts for a commodity supercycle are still intact, inflation is pushing higher, interest rates are likely rising, and pressures from geopolitics have put an emphasis on reliable suppliers like Canada. The apparent scramble for resources globally has made commodities valuable to the national security concerns of major economies and increased their importance as a diversifier for investor portfolios.

Alternatives

An allocation to alternative assets and investment strategies can benefit diversified portfolios when used over the long term. Given an increasingly uncertain outlook and high valuations in public stocks, we expect the need for additional diversification to benefit investment portfolios outside of traditional stocks and bonds.

Generally, liquidity has been strained among many alternative investment types. We view this as a function of:

- Where markets find themselves in the cycle for private credit and real estate, and

- The recent returns and income yields being seen in stocks and bonds.

Despite the reduced liquidity of various alternative investment types, the need for real diversification and uncorrelated income persists and may play a vital role when a correction in public markets occurs.

TriDelta Update

TriDelta recently updated our Estate & Donation Planner and partnered with a local hospital to help gauge the potential impact of charitable contributions on Canadians’ lifetime tax bill and final estate size. It’s a useful starting point for those interested and an important piece in determining whether donations fit your financial plan.

You can view the new calculator here: Donation Planner – TriDelta Private Wealth.

Looking Ahead

Whether it is rising inflation and interest rates, grappling with the increasingly high expectations for AI, or something new that surprises everyone, investors will have a lot to think about moving into the back half of 2026, much of it beyond anyone’s control. What can be controlled is our response to these developments. Investing can involve greed, fear, and plenty of extreme emotions where managing those emotions effectively is key to maintaining long-term discipline and protecting your financial goals.