Market Overview

As the old saying goes: “To the man with the hammer, everything is a nail.” With the U.S. once again picking up the proverbial hammer, we are seeing some similarities to the volatility seen in early 2025. If tariffs were the first nail, geopolitics has been the second as 2026 is once again being characterized by a U.S. policy decision leading to global uncertainty and stock markets struggling to find a direction. Despite Iran and the surging price of oil being the story in March, Artificial Intelligence (AI) was the main driver of negativity to begin the year as investor confidence in software companies reached its tipping point.

2026 has already been an eventful year for investors. In this review we share our perspective on the first quarter and the lessons that may guide what comes next.

- The Iran conflict and disruption to 20% of global oil supply sent energy prices surging with oil topping $100 – adding a level of geopolitical risk not seen since the early days of the Russia-Ukraine conflict.

- The global economy has shown an impressive ability to adjust to challenges and entered the year supported by government spending plans and the lagged effects of declining interest rates.

- While not all regions will be impacted the same by the Iran conflict, Canada and the U.S. are more insulated than most.

- Despite ongoing challenges from U.S. tariffs, Canada was a standout. The positive performance was supported by record energy exports and a better-than-expected domestic economy.

- Canada will face uncertainty as the July review of CUSMA approaches and headlines lead to sector specific weakness as investors digest the news.

- The Artificial Intelligence (AI) optimism that defined 2025 reversed as investors demanded evidence of profitability and grew wary of AI’s disruption on established industries.

- The reliance on only a handful of large stocks in the U.S. S&P 500 to decide overall market moves continues to make the case for greater diversification.

- Persistent inflation could be the issue that defines the decade as repeated policy moves from the U.S. stall progress globally and pose challenges for central banks.

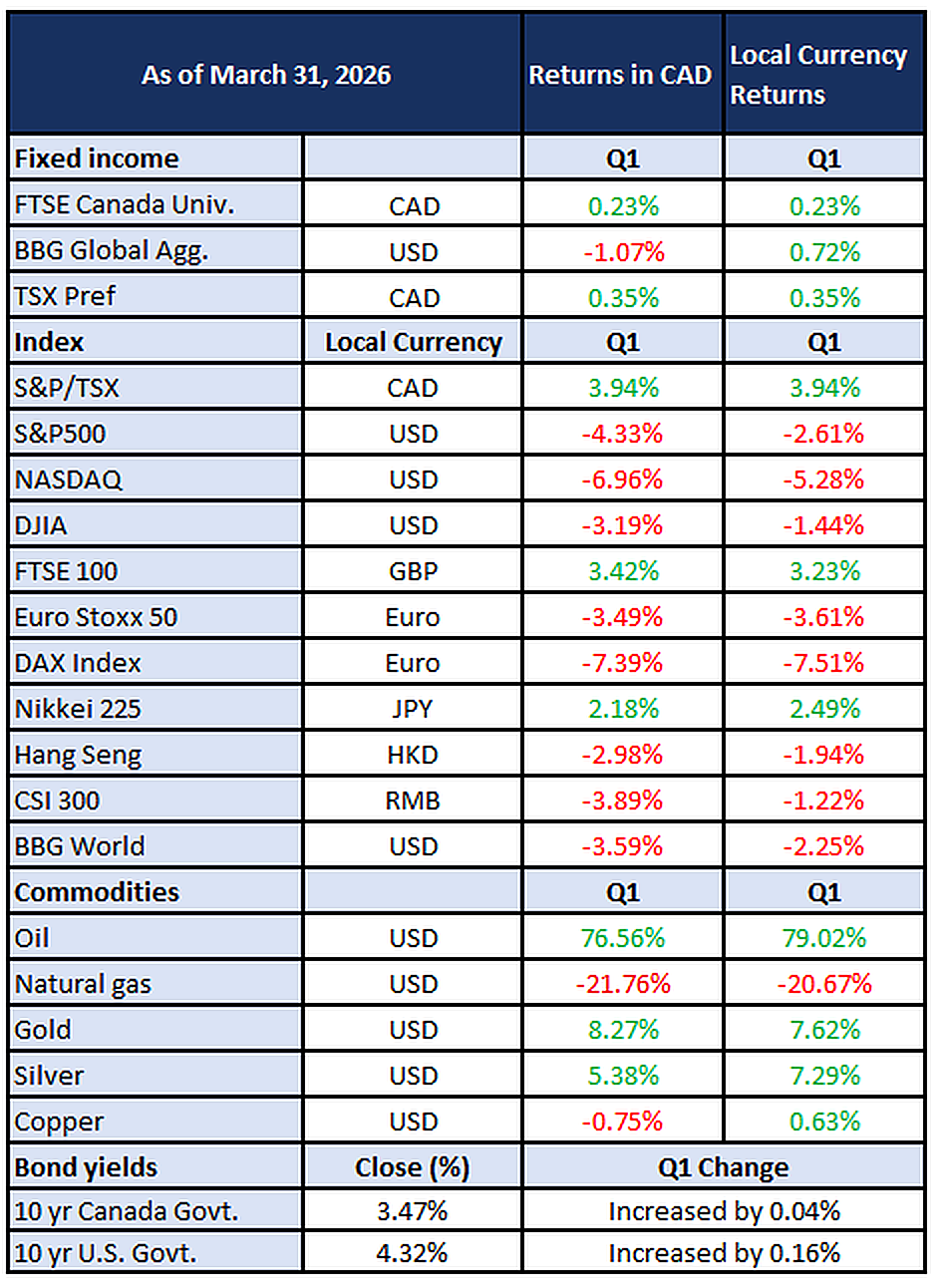

Market Returns

Too Much Little Oil

It wasn’t long ago that developments in Venezuela had investors thinking too much oil would drive prices lower. The latest, and evolving, developments in the Middle East are having the opposite effect with the global economy now grappling with surging oil prices after the narrow corridor which supplies one-fifth of the world’s oil is effectively closed.

At the time of writing, investors are betting on a resolution soon which would be positive for markets generally, but risks remain and it is helpful to look at past events to manage expectations.

Even when a resolution is reached:

- Higher energy costs could weigh on businesses and consumers, reducing the earnings potential for many companies.

- That said, the economy has proven resilient in recent years and it’s too early to tell if there will be widespread job losses — the hallmark of a recession.

- The backlog of ships could take weeks to clear even under ideal circumstances.

- Infrastructure damage has resulted in energy shortages across the globe and could take years to repair.

- Economies, particularly in Asia, are shell-shocked with some even facing shortages.

- There are real prospects that Iran will tax shipments through the strait indefinitely, creating a new constraint on the global supply chain.

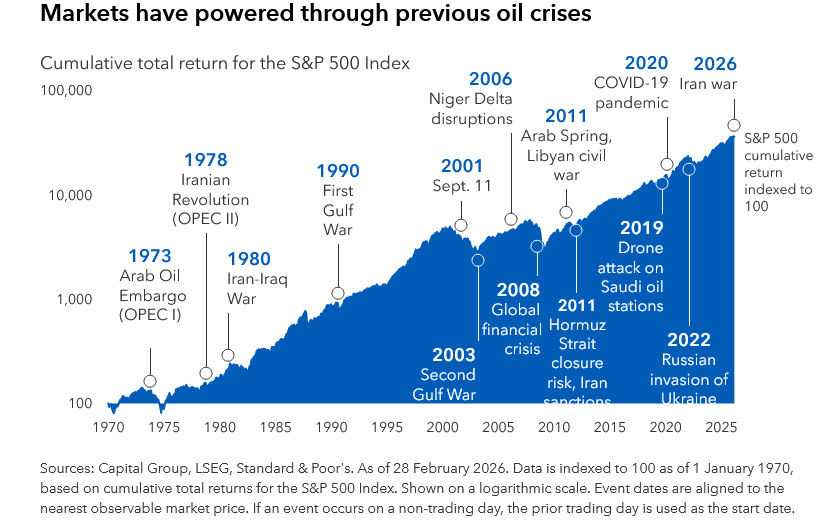

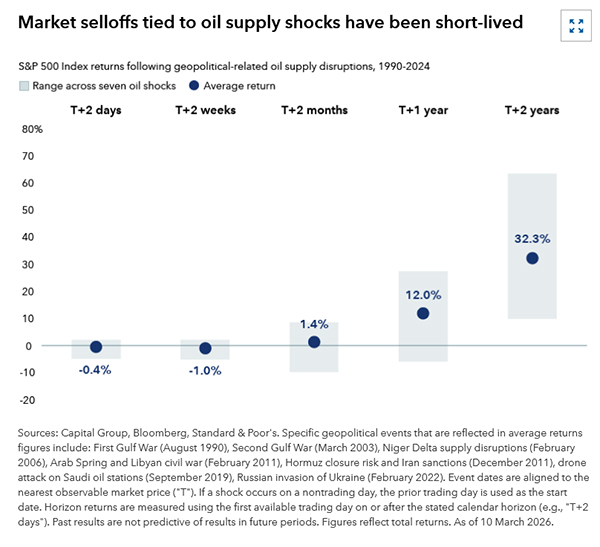

Historically, oil price spikes of 100% or more, sustained over a year, have been associated with recessions, making the duration of this conflict a key element of the longer-term consequences. While the most negative forecasts from the war may not come to pass, the shortages and price shocks will continue to be a prominent theme for investors to navigate in the months ahead.

Despite the uncertainty, there are lessons from prior years which may serve as a guide.

The world has demonstrated an ability to adapt to negative shocks, proven recently during the periods immediately surrounding the 2020 pandemic, Russia/Ukraine conflict in 2022, and the initial Trump tariff shock. It’s also important that investors stick with their long-term plans and remain invested as geopolitical events generally lead to brief periods of heightened volatility with past experiences proving these reactions tend to be short-lived.

There are also important differences from past energy shocks. Although it may not always seem this way, consumers spend less on energy than they did. The amount of household income that goes towards gasoline has fallen over the years, muting the impact of higher prices on total spending trends.

- It’s estimated that consumers spent the equivalent of 5.7% of their disposable income on gasoline, natural gas, electricity, fuel oil, and other fuels in 2024, down from a high of 10% in 1984.

Whether the market volatility of early 2026 might give way to smoother sailing is impossible to know, but the upcoming U.S. midterm elections could steer the Trump administration to focus on policies that inspire economic optimism. Regardless, prior episodes serve as a reminder that markets often absorb shocks faster than headlines suggest and recent developments seem to indicate a desire from the U.S. to find a resolution.

Artificial Intelligence (AI) & The Changing Reality for Tech Stocks

While not the dominant theme of the first quarter, there has been an undercurrent of concern among investors which we wrote about several times in 2025, a concern which became more widely held to kick off 2026. We can break this concern down into two, some may say, conflicting realities.

- AI stocks facing pressure to demonstrate profitability to justify the enormous spending.

- AI applications challenging established businesses – particularly those in software.

To begin the year, AI investors were already questioning the spending among the largest AI companies. We discussed this in our year-end commentary as investors lost patience and wanted to see tangible results.

- There will always be conflicting evidence of a bubble given most bubbles are only widely known in hindsight, but some of the data seems to contradict these fears.

- As of 2025, S&P 500 companies were spending about 86% of their cash flow. That’s significantly lower than the average pace of spending since 1962 and far lower than the levels seen during the dot-com bubble when many companies were spending 150% to 400% of cash flow.

While the concern among investors may still be justified, there is evidence that companies will listen to enough pushback. The early 2020’s “metaverse” served as an example that was expected to generate billions in revenues and even led Facebook to change their name to Meta. After lackluster returns and investor unease with spending, Meta wound up scrapping their metaverse plans in 2025.

The far bigger concern has been that the AI technology itself is challenging the business models of other industries, such as software, and raising questions about how they will be able to successfully navigate moving forward.

- Anthropic’s Claude is the main reason for the sell-off. The company announced new functionality in corporate departments like legal, sales and marketing, data analysis, productivity, finance and accounting.

- This was most felt by stocks like Salesforce and Microsoft with software stocks, in aggregate, falling more than 30%.

It’s no secret that AI is going to disrupt many businesses, but the speed of the sell-off may be assuming too much disruption in the near-term. Businesses evolve and not every company will come out a winner, but this isn’t the first major challenge facing technology companies.

- The advent of the internet made way for new huge players like Google while others shrank, went under, or were absorbed by others.

Some will falter, but others will adapt – integrating AI, innovating and strengthening their businesses. The near-term objective should be to position for transition rather than extinction and this is true in more than just software stocks. There is also evidence that more companies are participating in growing their revenues, a positive for investors, but it is still too early to say if we’re witnessing a true leadership change.

What we are doing and why

Stocks

Over the past three months, investors have navigated shifting expectations around interest rates, resilient corporate earnings, evolving global growth dynamics, and the risk of expanding global conflicts, all of which can influence which types of companies and investment styles outperform. Beginning the year, we adopted a cautious stance. Cash levels across the funds were elevated, as high as 11%, reflecting our view that valuations were expensive and that geopolitical risk was underappreciated.

That defensive stance paid off.

Both the Growth and Pension Funds outperformed during the quarter and spent the first two months benefiting from the selling of expensive areas of the market (AI/technology stocks) and buying of companies and sectors which have largely been underappreciated – areas of the stock market we already owned.

TriDelta Fund Performance — As of March 31, 2026

Moving deeper into the year, uncertainty will persist if the Iran conflict continues as the energy supply shock and associated inflation consequences intensify. That environment, while challenging, should provide opportunities for investors. For now, both the Growth and Pension Funds are emphasizing income-oriented companies, often carrying a dividend, and utilizing our elevated cash levels to pick up attractive companies at opportune times.

For an update on our current positioning, you can learn more about our strategies here:

The TriDelta team discussed our two funds in detail during a March 16th webinar. You can view the full recording here: Turning Volatility into Opportunity

Bonds

The uncertain backdrop for economic growth and rising inflation argues in favour of exposure to high-quality, short-term corporate bonds. That said, a selective approach to lower-quality bonds has rewarded investors in recent months.

- Bond investors have placed greater emphasis on the risk of rising near-term inflation rather than prolonged economic damage as surging energy prices have challenged expectations for central banks.

- Both the Bank of Canada and U.S. Federal Reserve have made clear that geopolitical risks add a layer of uncertainty but, for now, are unlikely to change interest rates.

- Currently, we do not think the conflict with Iran is enough, on its own, to drive increases in interest rates as slowing economic growth provides a counter to energy-related inflation.

- Evidence of elevated inflation is already visible as the Iran conflict drags out and will become clearer in the months ahead. However, the economic momentum to begin the year may help to absorb some of the near-term consequences.

- Generally, planned government stimulus may offer some support for consumers, though consumer confidence is another factor.

Preferred Shares

Canadian preferred shares were up marginally to finish the first quarter, rising 0.35%, in what ended as a relatively quiet start to the year with no new issuances and five redemptions. In the absence of more sizable redemptions, we expect preferred shares to perform more in line with broader stocks, while still benefiting from higher income.

Commodities

The beginning of the year saw wide swings for commodities which only increased as the Iran conflict progressed throughout March and into April.

- Precious metals such as gold and silver lost their shine after the momentum that pushed prices higher in 2025 began to stall.

- Despite this, the broader picture for gold remains supportive while industrial demand continues to be positive for silver.

- Concerns of prolonged supply disruptions drove oil prices higher.

- The eventual resolution of the conflict with Iran should prove a near-term risk to the high price of oil, however the destruction of oil assets in the gulf is likely to keep prices higher than before the conflict began.

Since 1950, Western nations have experienced stagflation (low growth, high inflation) about 23% of the time and saw commodities outperform stocks during these periods. While we believe a full-blown stagflationary shock like the 1970’s oil crisis to be unlikely, even mild stagflation warrants having an allocation to investments which may benefit in such a scenario.

Alternatives

An allocation to alternative assets and investment strategies can benefit diversified portfolios when used over the long-term. Given an increasingly uncertain outlook and high valuations in public stocks, we expect the need for additional diversification to benefit investment portfolios outside of traditional stocks and bonds.

Examples of alternative investments we use in portfolios include:

- Private equity; particularly in global infrastructure assets.

- Private lending to Canadian and U.S. businesses

- Music royalties

- Litigation financing

- Inclusive of law firm lending, injury settlement lending, and estate lending.

- Private real estate

- Inclusive of Canadian and U.S. apartment buildings, student housing, self-storage facilities, and new developments.

TriDelta Update

TriDelta is pleased to welcome Brian Peters as Strategic Advisor. Brian brings over 40 years’ experience in senior roles in the Canadian and U.S. Wealth Management industry, having most recently served as President and CEO of MD Financial Management. Prior to MD, Brian was President and CEO of RBC Dain Rauscher, the U.S. brokerage arm of RBC Wealth Management, leading a team of over 1,200 investment advisors. Welcome Brian!

Looking Ahead

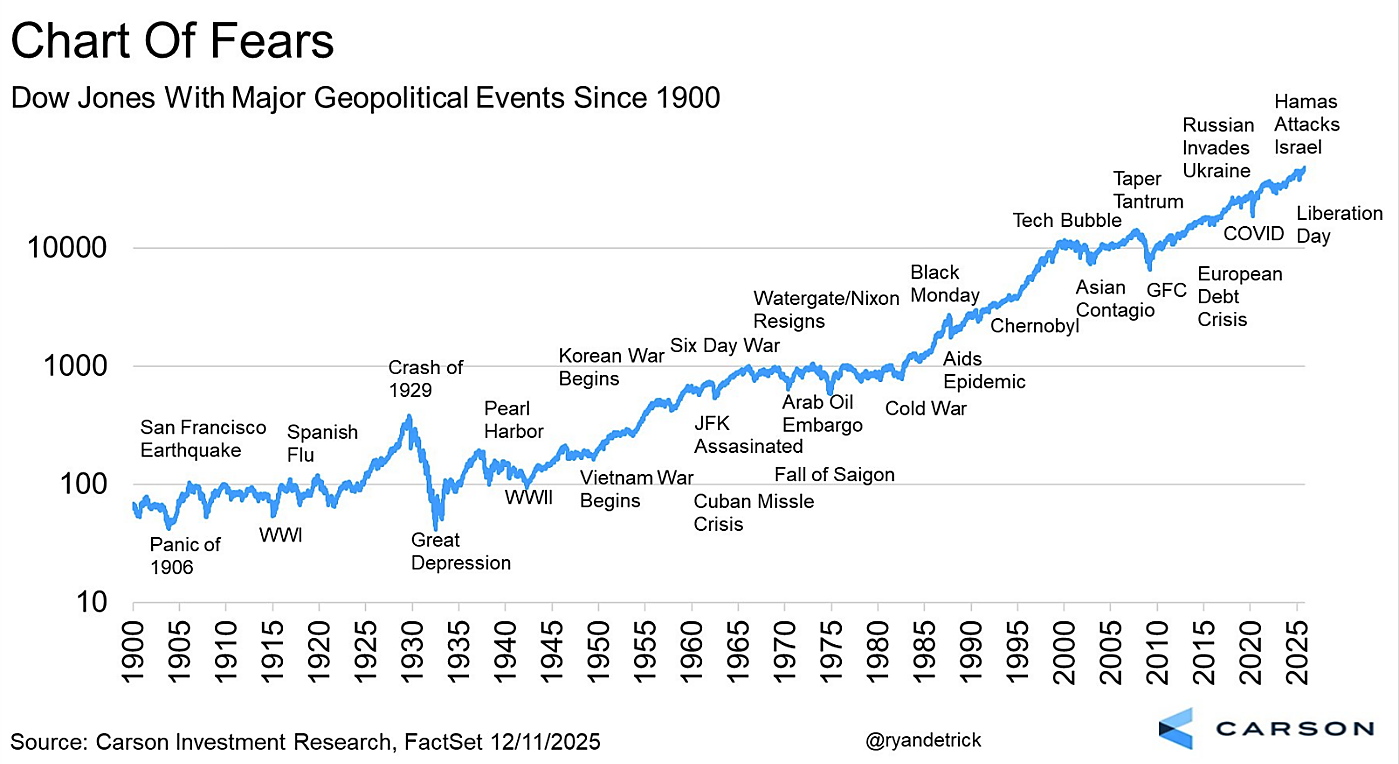

While what’s happening around the world can feel new or eerily similar to past events, stock market declines are regular occurrences. According to data from 1954 to 2025, markets generally experience declines of 10% or more once every 16 months and declines of 20% or more about once every six years. The reasons behind these declines have, at times, been justified while, during other periods, unjustified.

Regardless of the headlines driving this volatility, we have learned that:

- The more worried investors are, the easier it is for things to turn out better than initially expected.

- The fear generated by geopolitical events has, historically, almost always proven to be an opportunity for investors.

No one can say for certain what the future holds, but we have confidence in our ability to navigate what comes next by maintaining a prudent, diversified, and active approach to investing.